Mixed-use properties (buildings that combine commercial premises with residential accommodation)...

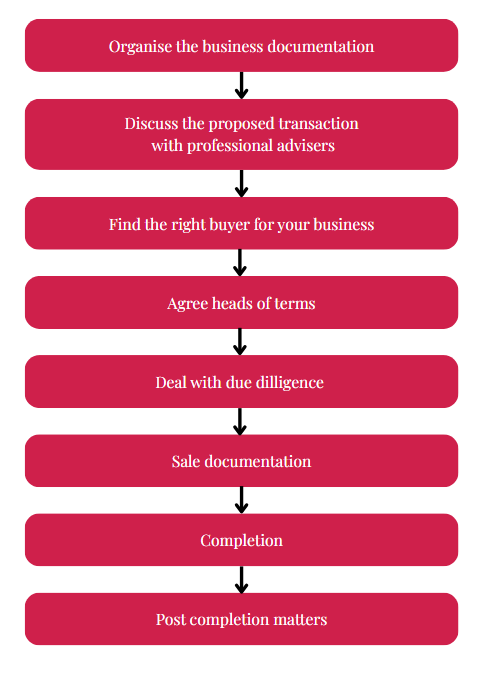

1. Organise the business’s documentation

Before selling a business, ensure the business’s records are in order. A buyer will want to confirm the history and records of the business are consistent, up to date and correct. This includes:

- up-to-date statutory books – including the register of members and the register of directors etc.;

- constitutional documents (e.g. articles of association, shareholders’ agreements etc.); and

- accessible copies of key contracts, property title documents and staff contracts.

A buyer will review these documents to understand liabilities and exposure and then decide if points need to be addressed to deal with any issues and shortcomings.

2. Find the right buyer for the business

Selecting the right buyer is essential for a smooth transaction. You’ll need to work closely with them throughout the process. The process will be so much better with the right support.

Additionally, consider:

- the buyer’s suitability for the company’s future;

- whether a handover or consultancy period is required for any sellers, ensuring a seamless transition of ownership, if any sellers are involved in management; and

- if the buyer has the necessary finance and backing to proceed with the proposed transaction.

A well-matched buyer benefits not only the sellers but the long-term prospects for the business. Corporate finance advisers, or business sales agents can play a crucial role in helping to find the right buyer.

3. Discuss the transaction with professional advisers

Consult your professional advisers to assess how to best structure the transaction. Early guidance can help streamline the process, avoiding pitfalls.

4. Agree Heads of Terms

Around the time that an offer is negotiated, heads of terms, or heads of agreement (Heads) outline the key points of the proposed sale, including:

- the sale price and payment terms (e.g. lump sum, deferred payments or an earn out);

- post sale restrictions; and

- any other specific sale conditions.

These initial terms guide the drafting of the main agreement, whether a share purchase agreement (SPA) or an asset purchase agreement (APA).

5. Deal with due diligence

Any diligent buyer will conduct a thorough review of the company through legal and financial due diligence. This might commence before an offer is made, and care should be taken to ensure that any sensitive information is protected.

To prepare for this, ensure that business’s documents are available and organised (preferably scanned, so they can be uploaded to a virtual data room). Information provided at this early stage of due diligence (usually, in a due diligence questionnaire) can assist with the preparation of the disclosure letter. The disclosure letter seeks to limit the seller’s liability (against warranties in the SPA/APA) by making relevant disclosures about the business.

6. Sale documentation

The core document to govern a business sale is an SPA or APA (referenced above). This incorporates the agreed Heads and other essential terms, such as warranties, indemnities and restrictions.

Ancillary documents are also usually required to execute the terms of the sale effectively (such as board minutes, stock transfer forms etc.).

7. Completion

Sometimes there might be a split between exchange and completion to enable conditions to be satisfied. However, it is preferable that signing of any purchase agreement and completion occur simultaneously.

At exchange - the sellers and the buyer will sign the documentation to effect binding agreement with the terms.

At completion - the formal transfer of ownership occurs and the purchase price that is payable at completion can be paid. This may involve various financing steps.

7. Post-completion matters

After completion, there are likely to be additional actions, including:

- filing updates with Companies House;

- arranging any necessary stamp duty payments; and

- managing transitional arrangements, such as providing agreed post-completion services, transferring operational passwords and handing over of equipment to the buyer (subject to the terms of the SPA/APA).

If a consultancy or handover period has been agreed, this typically begins immediately on completion to ensure a smooth transition.

Overall

Selling a business is a complex process requiring substantial preparation. Start planning early to facilitate a seamless transaction. While solicitors manage legal and transactional aspects, the seller’s concentration and input on operations and documentation is crucial for success.

Every business sale is unique, but by partnering with experienced corporate solicitors, such as our team, you can navigate the process effectively while minimising risks.

Please note that we do not provide tax advice. We strongly recommend consulting professional advisers before proceeding with any business sale process.